Monzo’s book of money: when a bank becomes a brand you want to visit

how Monzo’s soho pop-up turned a book launch into a brand experience

tldr: Monzo’s book of money pop-up shows how fintechs are rewriting the rules of what a bank can be. By making finance feel cultural, social, and worth lining up for, Monzo proved that the future of trust in money is built through experiences as much as interest rates.

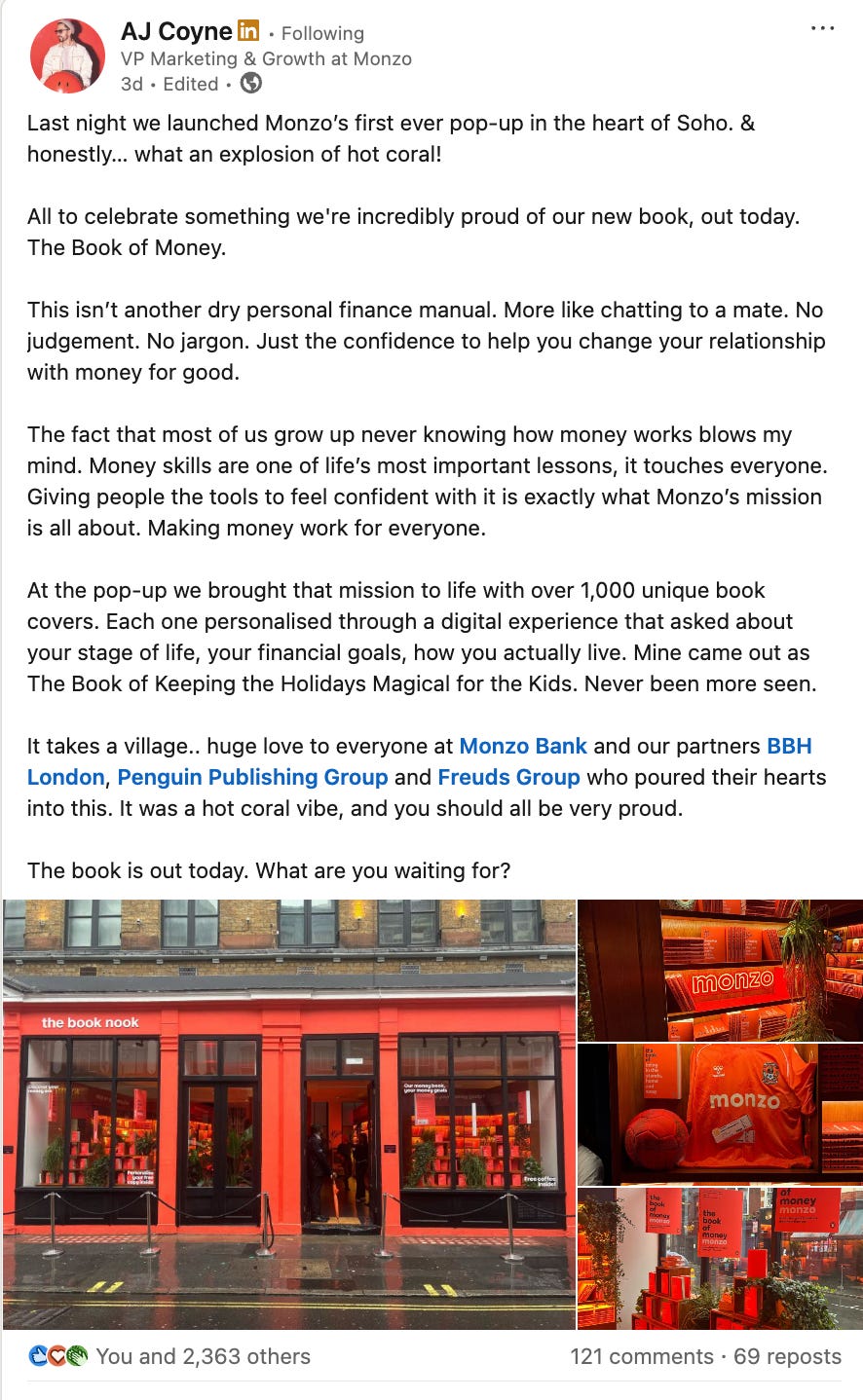

It was the morning of thursday 4 september when I spotted a post by AJ Coyne, Monzo’s marketing VP. The hot coral branding did its job of stopping me in my feed tracks and I found myself heading to Soho at lunchtime to see what the fuss was about.

There it was, the “book nook,” a coral emblazoned two-day pop-up that had drawn a queue snaking around the block. Wait time? Forty minutes to an hour. What were people waiting for?

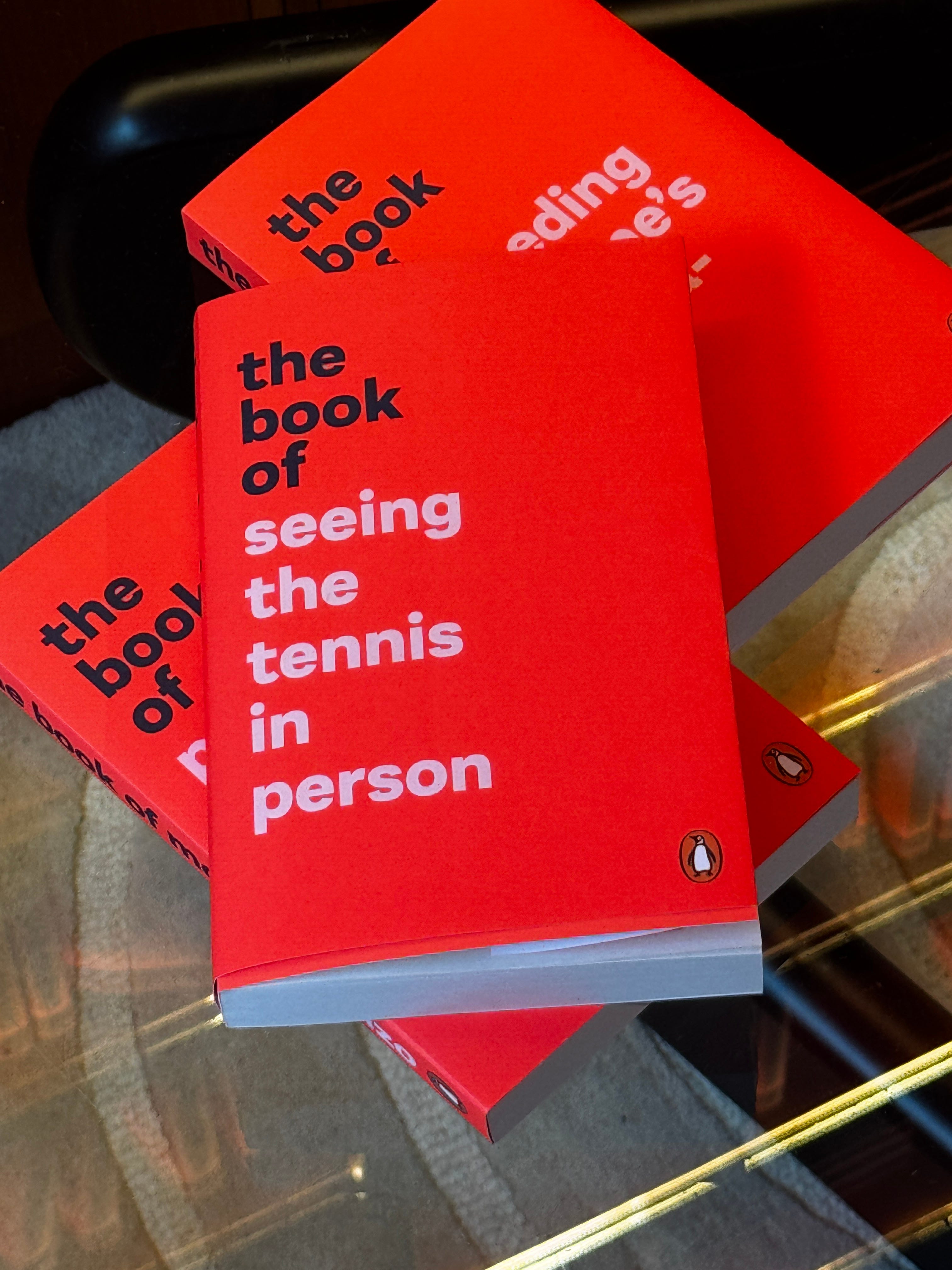

A tote bag of goodies: a personalised book of money published by Penguin, a branded pad and pen, a Monzo book as a bar of Tony’s chocolate, and free coffee inside. But there was more to it than merch.

This wasn’t your typical bank branch. It felt closer to a hype drop. Music, books stacked like sneakers, a barista and a Soho address that signalled cultural relevance. It was finance recoded as lifestyle.

So why is this interesting and why did I go?

Most banks traditionally would have wanted you to think about things like stability, compliance, security and reliability. While all those may still be true and important, Monzo wants you to think about something very different. Their book of money launch in Soho was not a corporate activation. It was a deliberate attempt to reposition the bank from a utility provider to a cultural player. More Spotify and less like an old and stuffy high street bank.

The pop-up itself felt closer to a design bookshop like Magma or a streetwear drop from Supreme or Palace than a financial brand event. There were stacks of books, hot coral accents, a DJ blasting out music, a barista serving free coffee and a Soho address. People were not coming to sign forms. They were coming to experience an idea: that money could be accessible, creative, and even enjoyable to talk about.

Why the placemaking mattered

Soho is not known as a place for banks. It is instead the beating heart of London’s cultural launches. It’s much more known for its bustling streetwear and sneaker drop culture with queues around the block for example, every Thursday for Supreme’s latest drop. By choosing Soho, Monzo placed itself in that same cultural background. A financial brand inserting itself into the logic of a streetwear drop was a deliberate and smart positioning shift.

From hot coral to hard cover

Monzo has always traded on taste and visual identity is key there. The hot coral debit card was a status signal in itself, spotted in bars and cafés like a badge of belonging. The book of money extends that trajectory. A card you carry in your pocket becomes a book you can hold in your hand. Both are symbols of identity as much as tools of utility.

Banks issue statements. Monzo published a book. The difference matters. Publishing a physical volume reframes the brand as more than a service provider. It positions them as a cultural authority on how people should think about money. In a world where financial literacy is a barrier and an opportunity, the book is education, trust building and marketing. It’s also a tangible bridge from digital to physical, giving Monzo tradition as well as novelty.

The cultural context

Monzo’s move sits within a wider trend of finance brands behaving like cultural brands.

Klarna partners with fashion houses to make “pay later” part of style, not just commerce.

Coinbase experimented with NFTs as cultural currency and doing their own pop up ‘trucks’ in NYC

Cash App sponsors hip-hop festivals and leans into rap culture.

The common thread is clear: finance is not just a utility. It is a stage for cultural relevance. Monzo’s Soho pop-up is another case study to add.

The tension

The risk is that this could feel like a quick hype blip. A two day splash and then reverting back to BAU. Money is a serious subject and education is needed from an early age. Why isn’t this taught in schools as a subject?

Turning it into a Soho moment could be dismissed as gimmick if it is not backed by deeper product innovation, deeper education and real consumer benefit. How is the book of money going to continue this over the months and years to come.

Legacy banks still dominate trust when it comes to mortgages, pensions, and savings. Monzo must prove that cultural capital can coexist with financial credibility.

The sensory shift

To me it was fresh, exciting, different, more cultural, more of an event. But it was only there for two days. What if this was a permanent fixture on the high street? What would they do there? They have an opportunity to become a hub for financial literacy but not in an old skool preachy way but with talks, workshops and mixers. It could also be a free drop in space for startups. All of it is purely educational and not salesy but heavy on culture. A bit like the vibe of The School of Life does but for money. And guess what that all does? Strengthens the brand, increases trust, affinity and loyalty.

The future signal.

If a bank can launch a book in Soho, what else could Monzo do? Start their own magazine? Run their own media brands, host cultural festivals, a startup investment fund or collaborate with design institutions? All of the above? The real signal is that financial brands are starting to compete not just on rates and products, but on taste, on style, in culture. Trust will increasingly be built through relevance and resonance, not only through regulation.

The Litman’s Lens View

Monzo’s book of money pop-up was more than a launch. It was a positioning masterclass and statement of intent: that the future of banking belongs to brands that can operate as cultural platforms. The Soho ‘shop’ made money feel less intimidating and scary and more tangible, creative, and even shareable. The move underlines a truth about modern finance: cultural capital is as important as financial capital. The banks that understand this will not just manage transactions. They will shape how we experience money itself.

PS. I still have my Mondo card!